Don’t Drive Into the Lake

Why blindly following the 4% rule can lead you off course

There’s a scene in The Office where Michael and Dwight are driving to a sales call.

They’ve struck out all day. This is their last stop.

Michael casually mentions it’s on the other side of a lake.

The GPS tells him to take a right.

Dwight says, “That can’t be right.”

Michael responds, “The machine knows,” and turns… straight into the lake.

It’s absurd. It’s uncomfortable. It’s hilarious.

And it’s not that far off from how people treat the 4% rule.

If you’re not familiar, the 4% rule comes from research popularized by William Bengen.

The idea is simple:

Withdraw 4% of your portfolio each year, and historically, your money would have lasted at least 30 years.

Through crashes. Through recessions. Through the worst markets we’ve seen.

It’s one of the most important anchors in financial independence.

But here’s what often gets missed.

Research from Michael Kitces shows the 4% rule isn’t just “safe.”

It’s often very conservative.

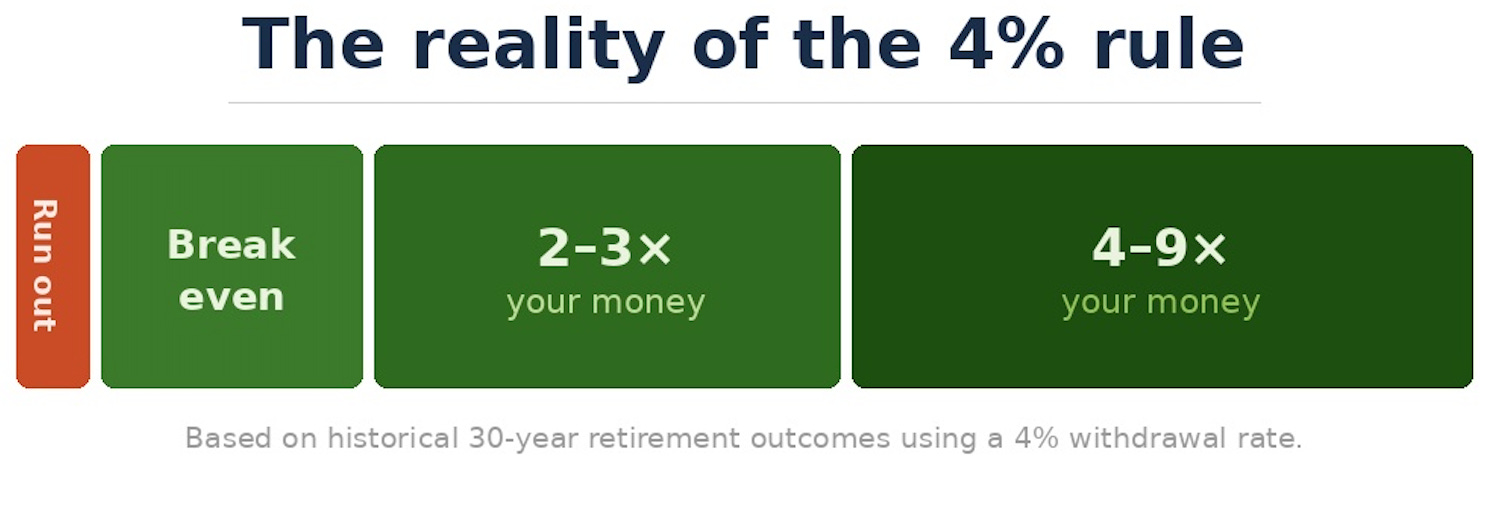

The chance of running out of money? ~3–5% historically

The median outcome? You spend for 30 years and still end with about 3x your starting balance

In best-case scenarios? 8–9x your money

And here’s the part that should stop you in your tracks:

You are roughly as likely to run out of money

as you are to end with 9x your money.

So what does that actually look like?

Here’s the reality:

A very small sliver where things go wrong.

A massive range where things go… really right.

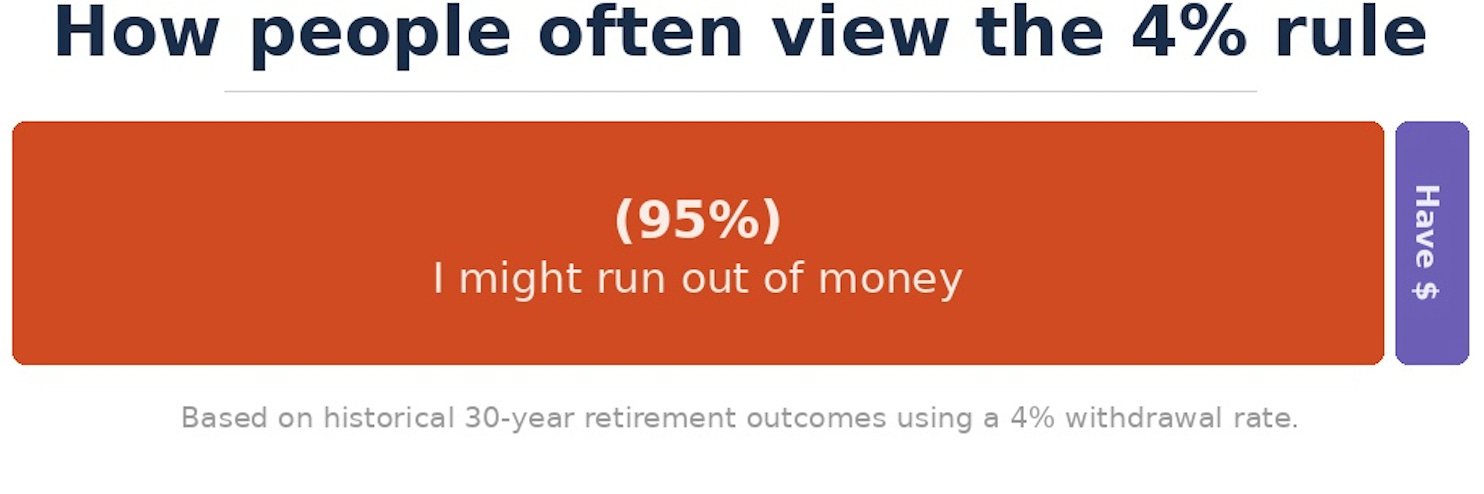

But that’s not how most people feel about it.

This is how people tend to see it:

Almost all the mental space goes to:

“What if I run out?”

And that fear makes sense.

This is your life, not a spreadsheet.

But here’s the key:

The 4% rule was never meant to be followed blindly.

It’s a guideline. Not a command.

Because in real life, you adjust.

If markets struggle, you spend less.

If things go well, you can spend more.

You don’t just keep withdrawing the same amount until you hit zero.

You don’t drive into the lake.

There are entire strategies built around this idea.

Flexible spending. Guardrails. Dynamic withdrawals.

Even Michael Kitces has shown that adjusting along the way can be more realistic than rigidly sticking to 4%.

The 4% rule is like GPS.

It’s incredibly useful. It’s based on a ton of data. Most of the time, it’s right.

But sometimes, you know something it doesn’t.

I skip my GPS’s suggested exit every morning because I know it backs up during school drop-off.

That’s the difference between following a rule and understanding it.

The 4% rule is a cornerstone of financial independence.

But it’s not something you blindly follow.

It’s something you use.

Adjust.

Personalize.

Because the goal isn’t to follow the rule perfectly.

The goal is to build a life where your money supports your time.

And don’t drive into the lake…

even if your GPS says to.